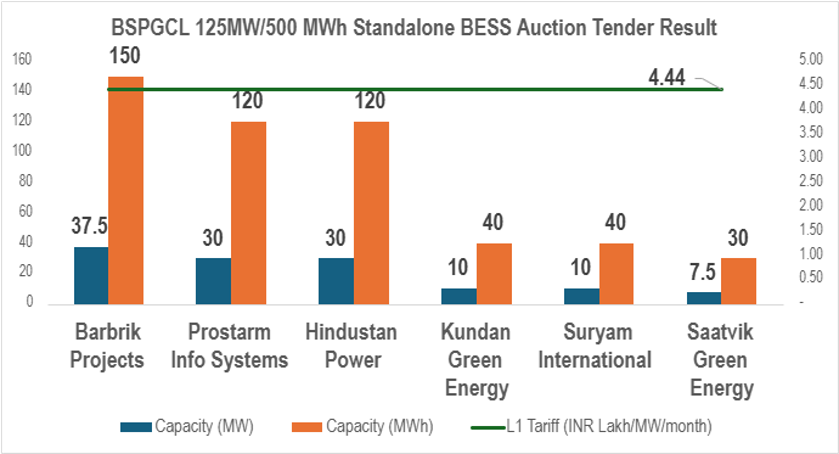

On July 2, 2025, the Bihar State Power Generation Company Limited (BSPGCL) awarded contracts for a 125 MW / 500 MWh standalone battery energy storage system (BESS) auction—one of the state’s largest storage procurements to date. Six developers won parcels of capacity, securing an identical L1 tariff of ₹4.44 lakh per MW‐month (~USD 5,180) under a 20-year Power Storage Service Agreement. The selected bidders and their allocations are:

Each successful bidder will receive Viability Gap Funding capped at ₹2.7 million per MWh (or 30% of capital cost) to help bridge financial viability, with projects required to commission within 12 months of the award. Facilities must connect at 33 kV and operate on “on‐demand” dispatch instructions from Bihar’s State Load Dispatch Center, ensuring seamless charging and discharging aligned with grid requirements

Building on Past Auctions: A Quick Look at Earlier BESS Results

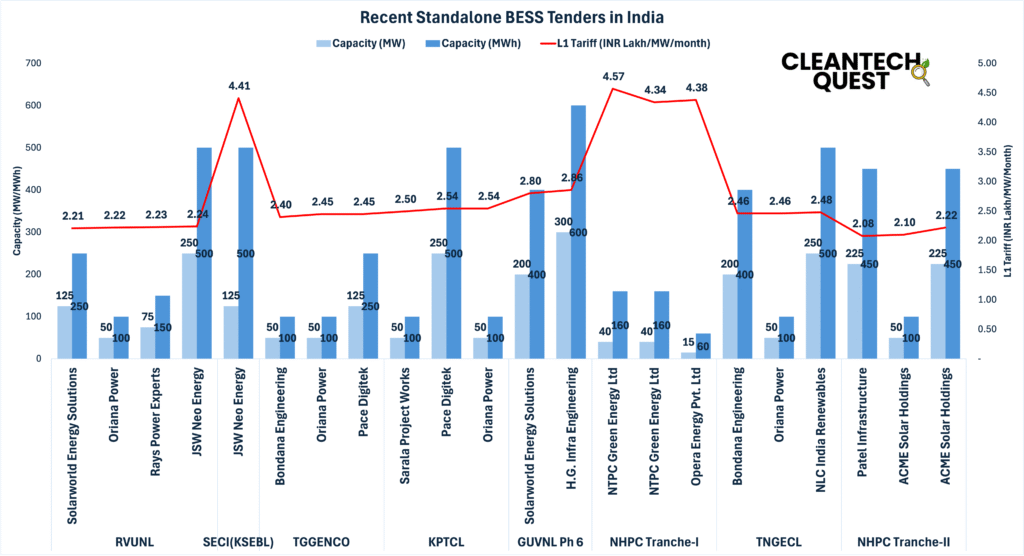

As India’s power sector grapples with ever-higher shares of variable renewable energy, 2025 has emerged as a watershed year for utility-scale battery energy storage system (BESS) procurement. Between January and June, seven major tenders totaling over 1.8 GWh of capacity were floated by MSEDCL, RVUNL, SECI (KSEBL), TGGENCO, KPTCL, GUVNL Phase 6, and NHPC (Tranches I & II). These auctions showcase two clear trends: an unmistakable slide in L1 tariffs toward the ₹2 lakh/MW-month range, and a steady 30% Viability Gap Funding (VGF) incentive anchoring project bankability.

Tariff Trajectory

At the start of 2025, MSEDCL’s 750 MWh auction attracted a lowest bid of ₹2.19 lakh/MW-month, closely followed by RVUNL’s 250 MWh parcel at ₹2.21 and ₹2.23 for smaller lots. Subsequent tenders in February and March saw a brief uptick—SECI (KSEBL) cleared at ₹4.41 and TGGENCO at ₹2.40–2.45—reflecting tight developer pipelines and equipment lead-times. By April and June, however, intensified competition among incumbents such as Pace Digitek, Oriana Power, Bondana Engineering, and ACME Solar drove tariffs back down to ₹2.08–2.54, with NHPC Tranche II’s Patel Infrastructure clinching a remarkable ₹2.08 lakh for 225 MW/450 MWh.

Financing & Policy Context

All six early-year tenders benefited from a uniform 30% VGF, underscoring MNRE’s commitment to de-risking storage investments. In contrast, late-phase auctions by GUVNL (Ph 6) carried 0% VGF, yet still achieved competitive bids at ₹2.80–2.86, demonstrating growing developer confidence and declining battery‐system costs. As transmission‐waiver extensions and pumped‐hydro mandates further bolster economic viability, 2025’s storage auctions highlight how policy calibration, market depth, and technological maturity are collectively compressing costs—paving the way for grid-scale BESS to support a 24×7 renewable future.

Strategic Implications and Outlook

A sub-₹5 lakh/MW-month tariff demonstrates that utility-scale BESS is rapidly reaching cost parity with traditional peaking plants—an essential milestone for enabling round-the-clock renewable power. Building on earlier multi-GWh deployments in Gujarat and Uttar Pradesh, Bihar’s recent auction further underscores how states are turning to storage to stabilize increasingly solar- and wind-dominated grids. This momentum has been fueled by a coordinated policy and funding framework—100% ISTS transmission-charge waivers, substantial Viability Gap Funding for up to 30 GWh, and clear dispatch protocols—paving the way for gigawatt-scale installations through 2028. With uniform, long-term dispatch contracts guaranteeing predictable revenue streams, both specialized BESS integrators and major power utilities are now lining up to invest in India’s burgeoning energy-storage market.