India’s renewable-energy (RE) generation surged in September 2025, reaching 48,382 million units (MU) including large hydro — a 12.6 percent year-on-year rise over September 2024, according to the Central Electricity Authority’s (CEA) Broad Overview of Renewable Energy Generation – September 2025. Excluding large hydro, RE sources contributed 26,064 MU, registering 16.4 percent growth and accounting for nearly 54 percent of total electricity generated that month.

Solar and Wind Lead the Growth Momentum

| Source | September 2025 (MU) | September 2024 (MU) | YoY Change |

|---|---|---|---|

| Solar | 13,556 | 11,303 | +19.9 % |

| Wind | 10,400 | 8,871 | +17.2 % |

| Biomass | 269 | 258 | +4.3 % |

| Bagasse | 105 | 119 | −11.2 % |

| Small Hydro | 1,494 | 1,613 | −7.4 % |

| Others (WtE/WHR) | 240 | 233 | +2.8 % |

India’s clean-energy growth continues to be powered by solar and wind. Together, these two sources contributed nearly 92 percent of total RE generation (excluding hydro) during September 2025.

Key highlights:

- Solar power generation rose to 13,556 MU from 11,303 MU, a +19.9 percent increase year-on-year.

– Expansion of utility-scale projects and strong irradiance across Rajasthan, Gujarat, and Karnataka supported the rise. - Wind power rose to 10,400 MU from 8,871 MU, up +17.2 percent, benefiting from the tail end of the monsoon in Tamil Nadu, Maharashtra, and Gujarat.

- Biomass and bagasse together contributed around 375 MU; biomass grew modestly while bagasse dipped as the sugar-crushing season ended.

- Small hydro generation softened to 1,494 MU (−7 percent YoY) due to uneven monsoon inflows.

Half-Year Trends Show Sustained Acceleration

Over the first half of FY 2025-26 (April–September), total RE generation excluding large hydro reached 166,863 MU, 23 percent higher than the same period last year. Solar and wind continued to dominate, accounting for >90 percent of this cumulative generation.

| Source | Apr–Sep 2025 (MU) | Apr–Sep 2024 (MU) | Growth (%) |

|---|---|---|---|

| Solar | 81,336 | 67,929 | +19.7 % |

| Wind | 72,744 | 55,888 | +30.2 % |

| Small Hydro | 7,378 | 6,641 | +11.1 % |

| Biomass & Bagasse | 3,944 | 3,357 | +17.5 % |

| Others (WtE / WHR) | 1,460 | 1,444 | +1.1 % |

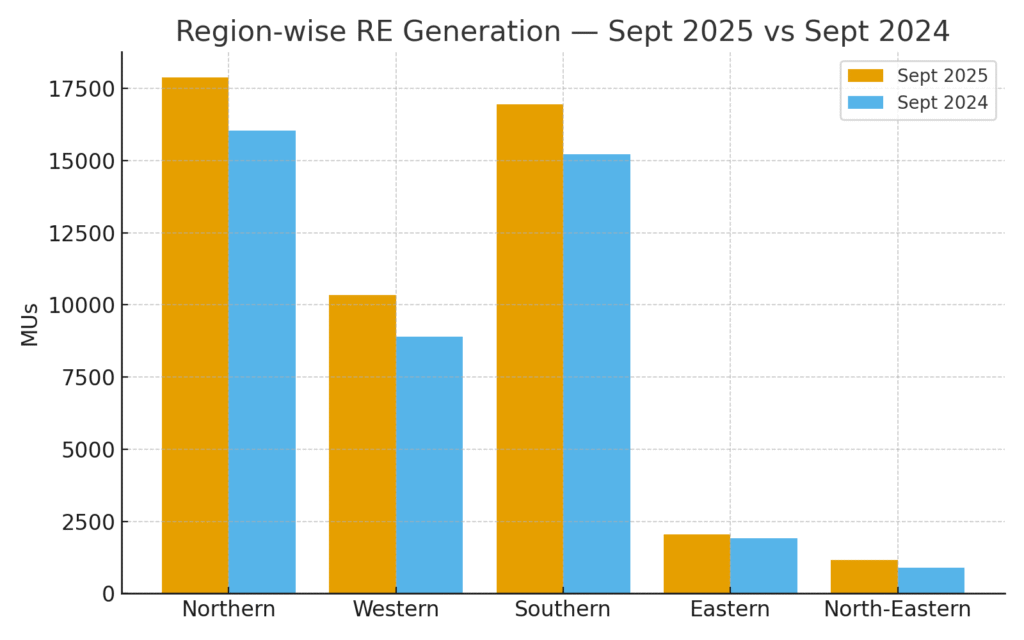

Region-Wise Performance

Regional snapshot (Sept 2025):

- Northern Region: 17,885 MU (+11.5 %) — led by Rajasthan’s solar and hydro inflows from Himachal Pradesh.

- Western Region: 10,348 MU (+16.1 %) — buoyed by Gujarat’s Khavda RE Park and hybrid plants in Maharashtra.

- Southern Region: 16,949 MU (+11.4 %) — continued strong wind generation in Tamil Nadu and Karnataka.

- Eastern Region: 2,036 MU (+6.2 %).

- North-Eastern Region: 1,164 MU (+31.8 %), a sharp rebound from a low 2024 base.

The Western and Southern regions together delivered over 55 percent of the country’s renewable-energy generation in September 2025.

RE Share in India’s Total Power Mix

- RE (excluding large hydro) accounted for 53.9 percent of India’s total generation in September 2025 — a milestone in the ongoing energy-transition trajectory.

- Including large hydro (22,317 MU), total RE stood at 48,382 MU, underscoring India’s steady shift toward low-carbon electricity.

Capacity Additions Reinforce Growth Outlook

During September 2025, India added 4,683.86 MW of new renewable capacity:

- Solar: 4,202 MW

- Wind: 443 MW

- Small Hydro: 25 MW

- Bio-Power: 14 MW

These additions strengthen supply availability ahead of the high-demand winter period and contribute to the 500 GW non-fossil target by 2030.

ISGS and CPSU Contributions

Inter-State Generating Stations (ISGS) accounted for 8,948 MU of generation (about 18.5 percent of total RE). CPSU-led projects, particularly NTPC’s Khavda, SECI’s Bhainsara and Shambu ki Burj, and NHPC’s Omkareshwar floating solar, continued to ramp up, improving the reliability and firm-power availability in the central grid.

Policy and Market Implications

- Balancing & Flexibility: Evening-ramp challenges highlight the need for dispatchable capacity and storage-linked PPAs.

- Transmission Readiness: High injections from Rajasthan and Gujarat demand faster rollout of Green Energy Corridors and new GNA-based scheduling frameworks.

- Tariff Design: With RE consistently above 50 percent of monthly electricity, time-of-day pricing and storage-linked markets are becoming essential.

- Investment Pipeline: Cumulative H1 data and September’s 4.7 GW additions indicate strong private-sector momentum ahead of FY 2026 auctions.

India’s renewable-energy expansion continues to break records — powered by solar scaling, monsoon wind recovery, and rapid CPSU commissioning. The challenge now shifts from capacity addition to integration, storage, and dispatch management to ensure 24×7 clean-power reliability.

With renewables already accounting for over half of India’s monthly generation, the September 2025 data reaffirm that the country is firmly on course toward its 2030 clean-energy goals.