As India closes calendar year 2025, the wind sector is back in focus—driven by a mix of fresh capacity additions, tighter quality controls for turbines, and renewed attention on offshore wind and repowering. While solar continues to dominate headlines, wind remains critical for balancing India’s renewable mix because it often generates in seasons and hours when solar output dips.

- Capacity growth: steady additions, with official data up to November

- Auctions and offtake: the pipeline is selective, not unlimited

- Policy and regulation: 2025 sharpened the “quality + reliability” agenda

- Offshore wind: slow start, but the roadmap is getting sharper

- The bigger picture: why wind matters in India’s 2030 grid

- Outlook for 2026: the “quality + bankability + hybrids” playbook

Capacity growth: steady additions, with official data up to November

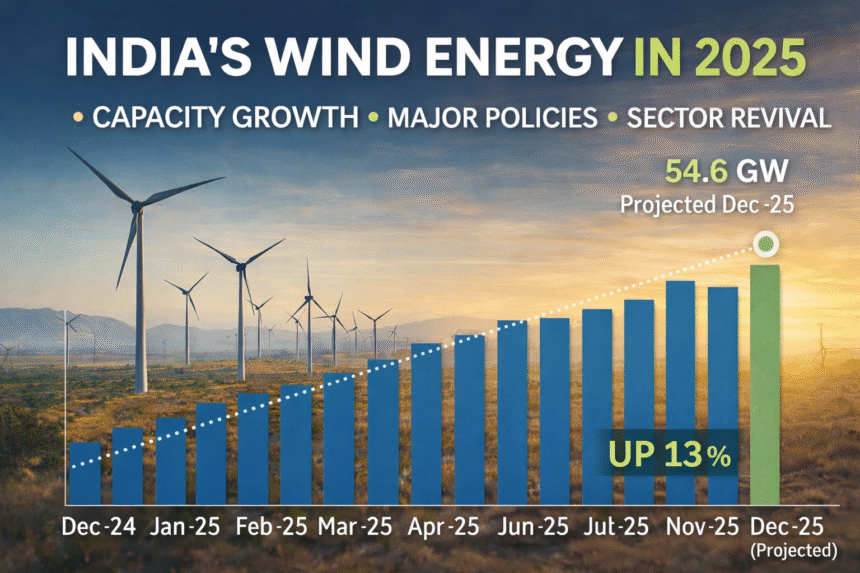

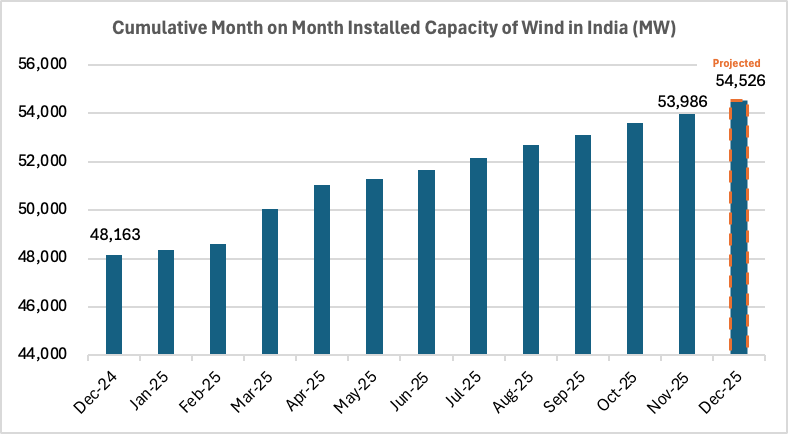

India’s cumulative installed wind capacity increased from 48.16 GW in December 2024 to 53.99 GW by November 2025, translating into ~5.8 GW of net additions within 11 months. The sector crossed the 50 GW milestone in March 2025, followed by consistent month-on-month growth through the rest of the year.

The pace of installations strengthened after Q1, reflecting improved execution on previously awarded capacities and better grid readiness in key wind states such as Gujarat, Tamil Nadu, Karnataka, Rajasthan, and Maharashtra. By November 2025, wind accounted for roughly 26–27% of India’s total renewable energy capacity, reinforcing its role as a complementary resource to solar.

This is a meaningful pace compared to the slower years wind saw earlier in the decade, and it signals that onshore wind is regaining traction in several key states. Sector trackers also projected that combined solar + wind additions could reach ~45–46 GW by end of 2025, indicating a strong year for variable renewables overall.

Auctions and offtake: the pipeline is selective, not unlimited

On the procurement side, wind auctions continued—but with a key reality check: not every tender is fully subscribed at desired tariffs and risk terms. For example, in SECI’s wind tender that was raised to 600 MW, only 300 MW was awarded, reflecting limited qualified bids under prevailing conditions.

This pattern highlights what developers have been saying: land availability, grid connectivity, payment security, and execution timelines matter as much as headline tariffs. For DISCOMs, wind remains attractive—but procurement design needs to keep risk allocation bankable.

Policy and regulation: 2025 sharpened the “quality + reliability” agenda

A defining feature of 2025 was the policy reset led by the Ministry of New & Renewable Energy (MNRE), aimed at improving turbine quality, manufacturing discipline, and long-term generation performance—areas that had previously affected investor confidence.

Key MNRE actions during the year included:

- Strengthening of the RLMM / ALMM-Wind framework:

MNRE amended procedures for inclusion and updating of wind turbine models, bringing greater clarity to certification, traceability, and eligibility norms. This move is critical for lenders and developers, ensuring that deployed turbines meet consistent performance and quality benchmarks. - Standardisation through SOPs for wind turbines and components:

Detailed standard operating procedures were introduced for listing not just complete turbines but also critical components, improving transparency across the wind supply chain and reducing execution and performance risks. - Revised guidelines for prototype wind turbine installation (June 2025):

These guidelines streamlined the process for installing and testing prototype turbine models, encouraging OEMs to introduce newer, higher-capacity machines for Indian conditions while maintaining regulatory oversight through NIWE. - Support for domestic wind manufacturing:

MNRE continued facilitation of concessional customs duty certificates (CCDCs) for wind turbine manufacturing, helping reduce input costs for domestic OEMs and supporting the broader Make-in-India objective for renewable energy equipment.

Collectively, these actions signal a clear shift: from capacity-only growth to quality-led, bankable expansion, aimed at ensuring that new wind capacity delivers reliable generation over its full life cycle. These measures strengthen standardisation, traceability, and credibility of turbine models deployed in India—crucial as turbines grow larger and projects move into more complex sites.

At the same time, India’s repowering conversation remains relevant. MNRE has an existing Repowering Policy (Dec 2023) that sets the direction for replacing old, low-capacity turbines with fewer, higher-CUF machines—especially in high-wind corridors where land is constrained. Repowering is not just about new MW—it’s about extracting more energy per hectare and improving grid-quality generation.

Offshore wind: slow start, but the roadmap is getting sharper

Offshore wind did not take off commercially in 2025, but the groundwork became more explicit. MNRE’s updated offshore wind approach is anchored in its revised strategy (Revision 02, 26 Sept 2023), which outlines multiple development models.

In 2025, offshore tenders faced setbacks—industry reporting notes that SECI’s offshore tenders were cancelled in August 2025 due to low developer interest, and the government is now looking to restart with improved data and packaging. News reports also indicated a Tamil Nadu offshore tender is being targeted around February 2026, supported by better wind assessment and potential viability support structures.

The offshore takeaway for 2025: India is still in “market creation” mode—working through resource certainty, risk sharing, evacuation planning, and Viability Gap Funding frameworks.

The bigger picture: why wind matters in India’s 2030 grid

As of November 2025, India’s renewable energy capacity stood at ~203.6 GW, with solar at ~132.8 GW, wind at ~54.0 GW, and large hydro at ~50.4 GW. With thermal capacity largely stabilising, grid flexibility is becoming the central challenge—and wind is increasingly valuable due to its seasonal and evening-hour generation profile, which offsets solar variability. Wind’s importance is also rising in hybrid and round-the-clock (RTC) renewable configurations, where combining wind, solar, and storage improves utilisation of transmission assets and enhances dispatchability.

Outlook for 2026: the “quality + bankability + hybrids” playbook

Going into 2026, the wind sector’s momentum will depend on:

- More predictable and bankable auction designs (offtake + execution risk)

- Faster grid readiness in high-wind states

- Repowering execution at scale

- Clearer offshore tendering structures

- Growing wind-solar-storage hybrids that stabilise generation and improve utilisation

In short, 2025 was a consolidation-and-rebuild year for wind—with steady capacity additions and stronger quality governance. If procurement and execution risks are addressed, wind can re-emerge as a high-confidence pillar of India’s clean power journey.